APR vs APY: What’s the Difference and How to Compare Returns

APR and APY often look interchangeable, but they measure interest differently. APR is the annual rate before compounding, while APY is the annual return after compounding is included. This guide breaks down the definitions, gives an example, and explains how these mechanics show up in KAST Earn.

Key Takeaways

- Annual Percentage Rate (APR) is the simple annual rate before compounding.

- Annual Percentage Yield (APY) is the effective annual return after compounding is included.

- In KAST Earn, yield is shown as APY because earnings are designed to compound into your Earn balance over time.

If you’ve spent any time comparing yields across crypto platforms, lending markets, or savings accounts, you’ve probably seen APR and APY used like they mean the same thing.

Someone quotes 4% APR. Someone else quotes 4% APY.

They look interchangeable. They are not.

Here’s the simple way to think about it:

APR is the base rate.

APY is what you actually get after compounding.

That does not mean APY is “better.” It means APY is the number that already includes reinvesting interest along the way.

Understanding APR and APY

APR (Annual Percentage Rate) represents the yearly interest rate without compounding. Think of it as the base annual rate.

APY (Annual Percentage Yield) represents the yearly return with compounding included. It is the effective annual return once interest is reinvested.

Traditional finance uses the same distinction. Borrowing products usually show APR because it describes the annual cost of borrowing. Savings products usually show APY because it reflects compounding.

APY is what happens when APR compounds.

APY = (1 + r / n)^n − 1

Where:

r = annual interest rate (APR)

n = number of compounding periods per year

This converts a simple annual rate into a compounded annual yield.

What Is APR?

Annual Percentage Rate describes the annual interest rate before compounding occurs.

It answers a simple question: if interest does not compound, how much would a balance grow over one year?

APR appears in many financial products including loans, lending platforms, staking markets, and credit cards. In lending products it may also incorporate certain fees associated with borrowing.

Simple way to read it:

If rewards did not compound, APR is roughly your annual return.

A product offering 5% APR would generate about $50 of interest on a $1,000 balance after one year, assuming nothing is reinvested.

What Is APY?

APY represents your return after compounding.

It reflects the base rate and how frequently interest is added back to the balance.

When rewards are added repeatedly, each addition slightly increases the base used to calculate the next reward. Over time, those small increases stack.

That does not mean compounding magically changes the strategy.

It means the math includes reinvestment.

APR vs. APY: What's The Difference?

The difference is compounding.

- APR assumes interest does not compound.

- APY includes the effect of reinvesting rewards.

As compounding frequency increases, APY rises relative to APR. Higher rates and longer time horizons make the gap more noticeable.

Here’s a simple rule that keeps you out of trouble:

If rewards are automatically reinvested, APY is closer to reality.

If rewards are paid out and not reinvested, APR may be closer to what you experience.

Compounding Example With $10,000

Assume you start with $10,000 and the annual rate is 4%. The only thing that changes is how often interest compounds.

Compounding simply means that earned interest is added back to the balance before the next interest calculation happens. When this occurs more frequently, the balance used to calculate the next reward is slightly larger each time.

Over a single day or month the difference is small. Over a full year, these small differences stack up.

The example below shows how the outcome changes depending on how often compounding occurs.

Even though the base rate stays the same, more frequent compounding slightly increases the final balance.

At lower rates the difference is small, but higher interest rates and longer investment periods can widen the gap.

How to Compare Interest Rates

When comparing yield opportunities, both numbers need to represent the same compounding assumptions.

Imagine investing $10,000.

Product A advertises a simple annual rate of 4%.

Final balance after one year: $10,000 × 1.04 = $10,400

Now consider a product that displays yield instead.

If the yield is 4%, the outcome would also be:

$10,000 × 1.04 = $10,400

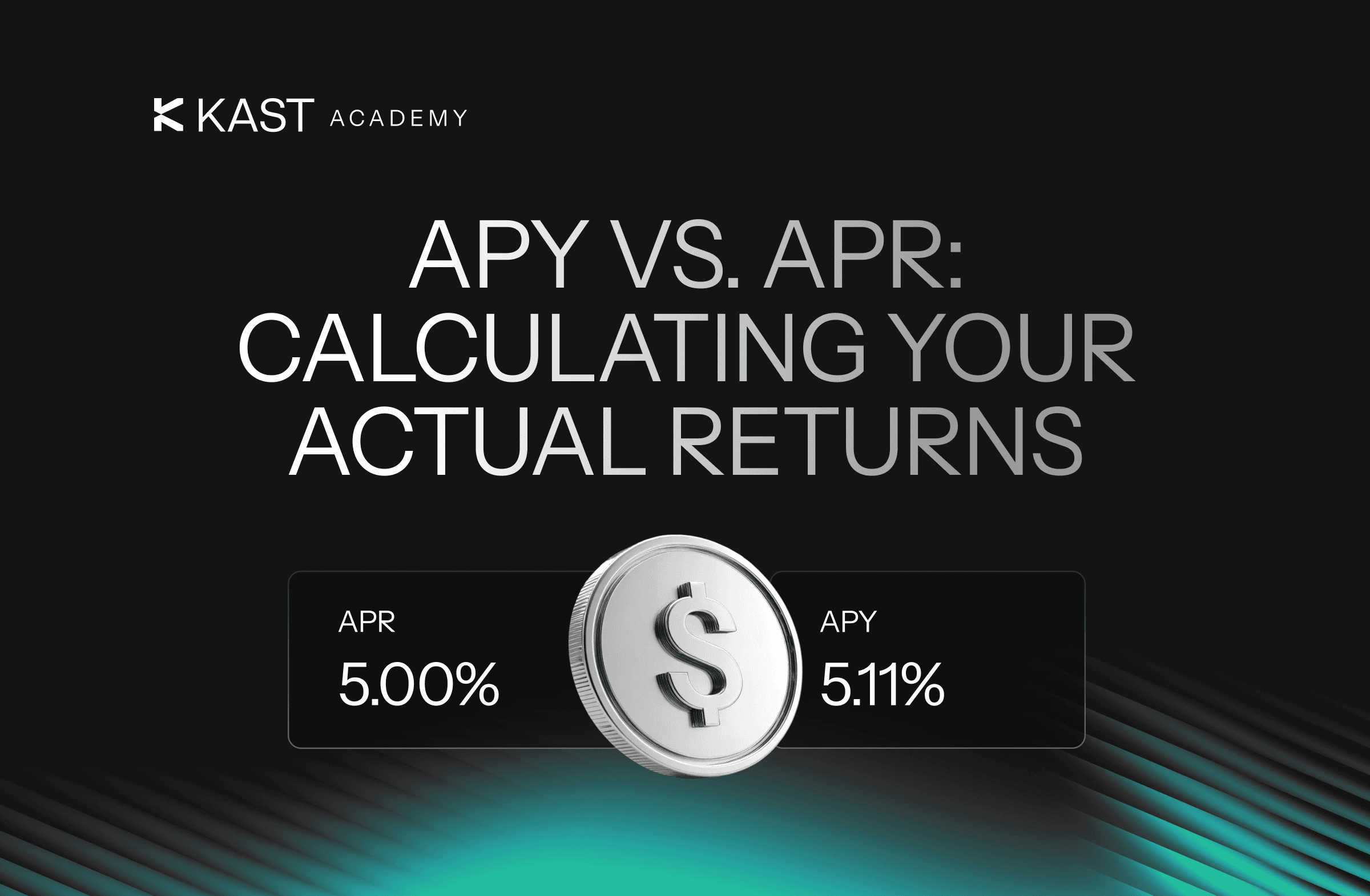

But if interest compounds monthly, the equivalent yield of a 4% base rate would actually be about 4.07%.

Using the conversion formula:

- APY = (1 + 0.04 / 12)^12 − 1

- APY ≈ 4.07%

This means a product advertising a 3.93%–3.96% APY with frequent compounding could generate nearly the same outcome as a simple 4% base rate without compounding.

Doing these calculations can help determine the cutoff point where the two approaches produce equivalent results depending on compounding frequency.

Key Definitions

How Yield Appears Inside KAST Earn

Inside KAST Earn, yield is presented as APY and the mechanics match that framing.

In practice, depositing USD in KAST Earn routes funds into the Gauntlet USD Alpha vault, a risk-optimized onchain vault designed to generate variable APY from onchain lending. The APY is flexible and moves with real-time market conditions.

The rate is variable and reflects the underlying onchain strategy and market conditions. Earnings compound automatically because rewards are continuously reinvested.

Instead of periodic interest payments appearing in your spending balance, your earn balance gradually increases and earnings are realized when funds move back to your spending balance.

The mental model is simple: auto-compounding yield that increases the balance over time.

Interpreting Interest Rates in Practice

APR and APY both describe annual interest rates, but they express them in different ways. The base rate shows the simple yearly return without compounding, while the effective yield reflects how balances grow when interest is reinvested over time.

When rewards compound automatically, the effective yield usually provides a clearer picture of real balance growth. Confusion typically arises when platforms present the two metrics inconsistently or when they are used interchangeably in discussions about yield.

Once the distinction is understood, comparing financial products and evaluating returns becomes much more straightforward.

Disclaimer: This content is provided by KAST Academy for educational purposes only and is not intended as financial advice or a recommendation to engage in any transaction. All information is provided "as-is" and does not account for your individual financial circumstances. Digital assets involve significant risk; the value of your investments may fluctuate, and you may lose your principal. Some products mentioned may be restricted in your jurisdiction. By continuing to read, you agree that KAST group, KAST Academy, its directors, officers and employees are not liable for any investment decisions or losses resulting from the use of this information.

Related articles

Where Does Stablecoin Yield Come From?

Stablecoin yield comes from real onchain demand, borrowing, trading, and capital deployment, not inflation or promos. When demand rises, yields rise. When it falls, so does yield.

Staking vs. Lending: A Beginner’s Guide to Safer Yield

Staking and lending can look similar in crypto, but they work for very different reasons. This guide breaks down how yield really works, what can fail, and how to choose the safer strategy for your situation.

What Is RWA Backing? Tutorial on How Treasury Bills Secure Your Yield

Real-World Assets (RWAs) bring familiar assets like U.S. Treasury bills and bonds onchain. RWAs let you earn yield backed by traditional financial instruments. This guide explains how RWA backing works, why it exists in crypto, and how KAST Earn uses it to help you generate steady yield.