How to Keep Up With Inflation: Holding Stablecoins vs. Holding Fiat Currency

If prices rise faster than your money grows, purchasing power quietly erodes. This guide explains how inflation works and walks through the main ways people keep up with it using both fiat and crypto. You will see how tools like index funds, bonds, commodities, and stablecoin yield generate returns.

Key Takeaways

- Inflation quietly reduces purchasing power when your money earns less than prices rise.

- “Beating inflation” usually means owning assets or strategies with returns that can keep up over time, with real trade-offs.

- Stablecoin yield can be a practical tool for idle USD, and KAST is built to make accessing it simpler without turning it into a second job.

Your money sits safely in a bank account. But everything you buy costs more. You did the responsible thing. Yet you're still losing purchasing power.

That reaction makes sense.

Inflation is not a line item you approve. It is something that happens to your purchasing power when your money sits still.

Inflation refers to a sustained rise in the price level of goods and services across an economy, which means the same amount of money buys fewer goods and services over time.

This guide walks you through two parallel toolkits: the traditional (fiat) ways people try to keep up with inflation, and the crypto ways people try to do the same thing using stablecoins and onchain yield.

Then it will show how people use tools like KAST Earn to try to keep up with inflation, with clear trade-offs and real risks.

No hype. No “guaranteed.” Just mechanisms and trade-offs.

What Is Inflation?

Inflation is the rate at which consumer prices rise across an economy over time, increasing the overall price level and reducing the real value of money.

Economists usually group inflation into three broad types based on what drives price increases.

Measuring Inflation

Central banks typically target a 2% annual inflation rate. Rates above this threshold reduce purchasing power faster.

Monetary authorities like the Federal Reserve within the federal reserve system use monetary policy tools such as raising interest rates to maintain price stability and maximum employment.

Economists track inflation using several inflation measures such as the Consumer Price Index (CPI), the Producer Price Index, and the GDP deflator, each tracking the percentage change in a basket of consumer prices.

The CPI has increased by 36% between March 2016 and 2026, equivalent to an average annual inflation rate of about 3.1%.

This is why “holding cash” can be a losing strategy in the long-term.

Not because cash is “bad.”

Because cash holds its same value while most assets increase in price.

If the inflation rate rises faster than nominal interest rates, the nominal rate minus inflation becomes negative, which has negative effect on the purchasing power of savings.

There is no single perfect inflation hedge, which is why diversification keeps coming up in serious discussions.

How To Keep Up With Inflation Using Fiat

Many countries experience different inflationary pressures depending on economic growth, money supply changes, and interest rates set by central banks.

When people say “beat inflation,” they usually mean holding assets that give a return that either keeps up or increases faster than inflation.

Here are five common ways people try to do that using traditional financial tools.

1) Buy Indices

If you want broad exposure without picking individual winners, index funds (or ETFs) are the default option many long-term investors use.

The reason indices show up in inflation discussions is simple: a broad basket of companies can raise prices, grow earnings, and compound over time. That does not mean the ride is smooth. It means the mechanism can keep pace over long horizons.

The S&P 500 has increased by about 230% between March 2016 and 2026, which corresponds to an average annual return of roughly 12.7%.

*Note: Past performance is not indicative of future results.

As seen in the previous chart, the consumer price index has increased by only 36% during this time, so over that period, the S&P 500 outperformed CPI.

The trade-off is that indices can still drop hard in the short term, despite their consistent long-term returns.

2) Buy Bonds

Bonds are often used for stability and income, but the inflation rate changes the math.

Traditional fixed-rate bonds can lose value when interest rates rise. Inflation-linked bonds like Treasury Inflation-Protected Securities (TIPS) are designed to adjust with inflation, which is why they are frequently mentioned as a direct inflation hedge.

While the 10-year U.S. government bond currently gives 4% annual return, it has given an average of roughly 2.8% since Mach 2016. Hence, with its roughly 31.6% increase over the past ten years it has not beaten the CPI increase.

The trade-off: bonds can be lower volatility than stocks, but the return ceiling is often lower too, and inflation can still erode returns if you are not choosing instruments designed to respond to it.

3) Buy Stocks

Owning individual stocks is the “high-conviction” version of the inflation defense story.

Companies with pricing power can sometimes pass higher costs onto customers, which can help earnings hold up in inflationary environments.

The trade-off is obvious: concentration risk.

You can outperform. You can also underperform badly. Even if your inflation thesis is right.

4) Buy Commodities

Commodities and gold often surge when the inflation rate rises.

They can help diversify an inflation-defense mix, especially in certain regimes.

The price of Gold has increased by a massive 315% between March 2016 and 2026, handily beating inflation, the S&P 500 and the return of the 10-year U.S. Government Bonds.

The trade-off is that commodities can be volatile and inconsistent over long periods. This is usually a “portion of a portfolio” tool, not a single plan

Fiat Summary Table

How To Keep Up With Inflation Using Stablecoins?

Stablecoins are designed to hold a stable value, usually around $1. That makes them a convenient base layer for earning yield.

Yield represents payment for a specific financial service or risk.

So if you are looking at an APY, the useful question is not “how high is it?” It is: what activity is generating that yield?

Stablecoin yield is not guaranteed. Rates can change, and you can lose money. Stablecoins and onchain strategies involve risks, including smart contract failures, liquidity constraints, and stablecoin depegging.

1) Staking

Staking exists because proof-of-stake blockchains pay participants for helping secure the network.

Validators process transactions and maintain the chain. Delegators can stake their tokens with validators and share in those rewards.

That’s where staking yield comes from.

While staking rewards differ from stablecoin yield, many platforms present both as 'earn' options.

The trade-offs are straightforward.

You earn network rewards, but you are still exposed to token price volatility, validator performance, and sometimes unstaking delays during periods of market stress.

Rewards also vary depending on network conditions, validator fees, and how much total capital is staked across the network. So even staking yields move over time.

- Market Cap

- Total Supply

- 24h Volume

- Peg

- Avg Deviation

- Collateral

- Cash, US Treasuries + Assets

- Governance

- Centralized

- Funds Freezable

- Yes

- Issuer

- Tether Limited

- Jurisdiction

- British Virgin Islands

Historical Incident: Tether has faced scrutiny regarding the full backing of its reserves.

Live market data sourced from DefiLlama (opens in new tab) and CoinMarketCap (opens in new tab)

2) Lending

Lending is the cleanest stablecoin yield model.

Borrowers want stablecoins for trading, leverage, or liquidity. They post collateral and borrow against it. Then they pay interest.

Suppliers earn a portion of that interest.

Platforms like Aave, Compound, and Morpho run these lending markets.

Rates change because demand changes. When traders want leverage, borrowing demand rises and yields increase. When markets slow down, yields fall.

Most lending protocols require borrowers to post more collateral than they borrow, which is what protects lenders if markets move quickly.

The trade-offs are mostly technical: smart contract risk, liquidation mechanics, and liquidity risk if many users withdraw at once.

Read our full guide on staking vs lending.

3) DeFi Liquidity Pools

Liquidity pools power decentralized exchanges.

If you provide assets to a pool, traders pay swap fees, and liquidity providers earn a share of those fees.

The complication is called impermanent loss.

Impermanent loss happens when the prices of the assets in the pool move relative to each other. Automated market makers rebalance positions as prices change, which can leave liquidity providers with a different mix of assets than they started with.

Sometimes trading fees offset that effect.

Sometimes they don’t.

The risk becomes more noticeable when the two assets in a pool move very differently in price, which is why stablecoin pairs tend to experience less impermanent loss than volatile token pairs.

If your goal is preserving purchasing power with minimal management, this is usually not the first strategy people choose.

Read our full guide on impermanent loss.

4) Tokenization And RWA-Backed Yield

Another approach brings traditional financial assets onchain through tokenization.

These are known as real-world assets (RWAs).

One common example is tokenized U.S. Treasury bills, where stablecoins are allocated into instruments that generate interest in traditional markets.

The yield comes from government bond interest rather than trading activity or leverage.

This is why RWA-backed yield tends to look more familiar to traditional investors. The underlying asset is the same; the difference is that access and settlement happen onchain.

The risks shift accordingly.

Instead of focusing on trading mechanics, the main considerations become legal structure, custody, redemption liquidity, and smart contract infrastructure.

For a full guide on tokenization and how Treasury Bills secure your yield, click here.

Stablecoin Summary Table

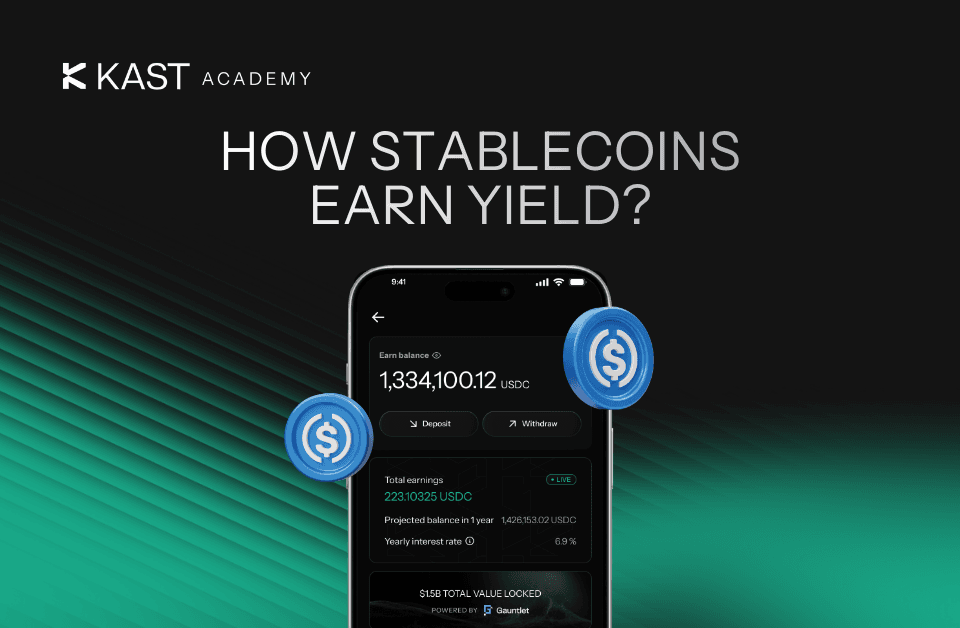

KAST Earn

Once you understand the mechanisms, the practical question becomes simple.

How do you access stablecoin-style yield without turning it into a second job?

That’s what the Earn program in KAST is designed for.

Stablecoin yield comes from real activity. Borrowers paying interest. Traders paying fees. Capital being deployed into strategies that generate returns.

- Market Cap

- Total Supply

- 24h Volume

- Peg

- Avg Deviation

- Collateral

- Cash + US Treasuries

- Governance

- Centralized

- Funds Freezable

- Yes

- Issuer

- Circle

- Jurisdiction

- United States

Live market data sourced from DefiLlama (opens in new tab) and CoinMarketCap (opens in new tab)

It isn’t free money, and the rates move with supply and demand. When stablecoins are in high demand, yields rise. When demand cools, they fall.

KAST Earn routes eligible USD into a managed onchain strategy, so you can participate in that yield without manually managing lending positions or liquidity pools.

*Note: Returns are not guaranteed and rates vary with market conditions.

Two things are worth knowing upfront: the APY is variable, and earnings are auto-compounded.

Instead of receiving daily interest payments, the value of your Earn balance gradually increases, and you realize the gains when you withdraw back to your spending balance.

The goal is not to turn you into a DeFi operator.

It is to make stablecoin yield more accessible, with fewer steps and less ongoing work.

Ultimately, inflation expectations shape how investors, businesses, and policymakers respond to rising prices, and they often influence future monetary policy decisions.

What Helps Keep Up With a High Inflation Rate?

Inflation does not need you to panic.

It just needs you to stay passive.

The fiat toolkit and the stablecoin toolkit are trying to solve the same underlying problem: keep purchasing power from eroding.

In fiat, that often means some mix of indices, bonds, real estate, and diversifiers like commodities.

In crypto, it means understanding what yield is actually coming from, then choosing trade-offs you can live with.

You should not have to become a full-time portfolio manager just to stop your money from slowly losing ground.

Now you do not.

Disclaimer: This content is provided by KAST Academy for educational purposes only and is not intended as financial advice or a recommendation to engage in any transaction. All information is provided "as-is" and does not account for your individual financial circumstances. Digital assets involve significant risk; the value of your investments may fluctuate, and you may lose your principal. Some products mentioned may be restricted in your jurisdiction. By continuing to read, you agree that KAST group, KAST Academy, its directors, officers and employees are not liable for any investment decisions or losses resulting from the use of this information.

Related articles

Where Does Stablecoin Yield Come From?

Stablecoin yield comes from real onchain demand, borrowing, trading, and capital deployment, not inflation or promos. When demand rises, yields rise. When it falls, so does yield.

Staking vs. Lending: A Beginner’s Guide to Safer Yield

Staking and lending can look similar in crypto, but they work for very different reasons. This guide breaks down how yield really works, what can fail, and how to choose the safer strategy for your situation.

What Is RWA Backing? Tutorial on How Treasury Bills Secure Your Yield

Real-World Assets (RWAs) bring familiar assets like U.S. Treasury bills and bonds onchain. RWAs let you earn yield backed by traditional financial instruments. This guide explains how RWA backing works, why it exists in crypto, and how KAST Earn uses it to help you generate steady yield.