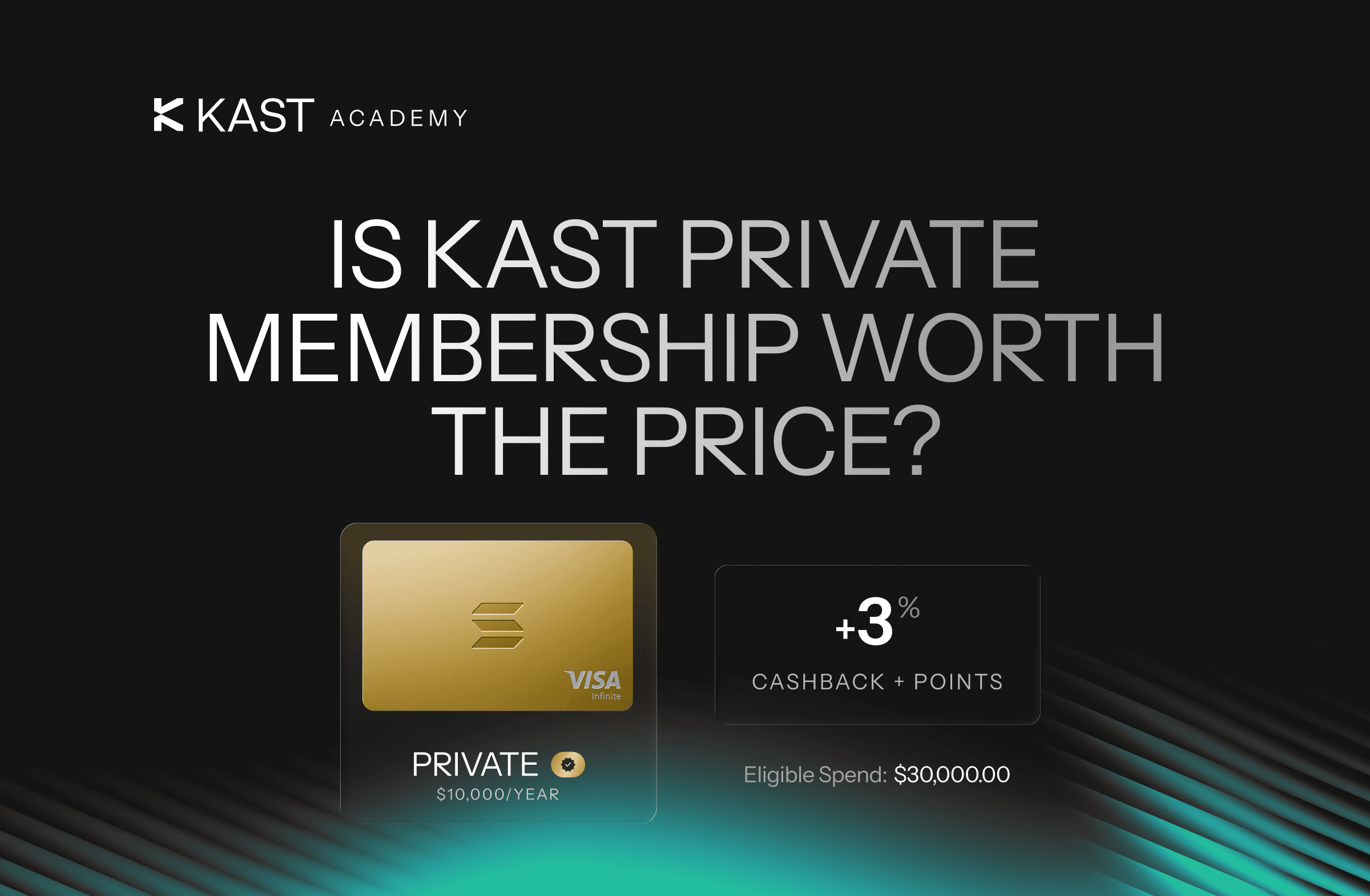

Is a $10,000 Membership Worth It? Calculating the ROI of KAST Private

KAST Private offers 3% cashback and extra rewards, but it only pays off if your spending is high enough. Here’s the exact break-even point and how to decide if the $10,000 membership makes sense for you.

Key Takeaways

- Private is a rewards tier for your whole KAST account, not a single card, so the decision comes down to whether your spend can use the higher ceiling.

- On cashback alone, Private breaks even at about $333,333/year of eligible spend, or ~$27,778/month at a 3% rate.

- Above break-even, cashback turns positive, and KAST points add value on top, but the decision starts with the cashback baseline.

You’re looking at a $10,000 KAST Private membership and asking the only question that matters:

Is this worth it, or will my money go to waste?

Fair question.

Before you run the numbers, you need to understand what KAST memberships actually are and what Private changes.

What Are KAST Memberships?

KAST memberships are tiers.

Each tier sets the rules for your entire account, not just one card. Every card you use, virtual or physical, follows the same structure.

Your tier controls:

- Your cashback rate

- Your annual fee

- The perks attached to your account

So when you choose a tier, you’re not picking a card. You’re defining how your whole account works.

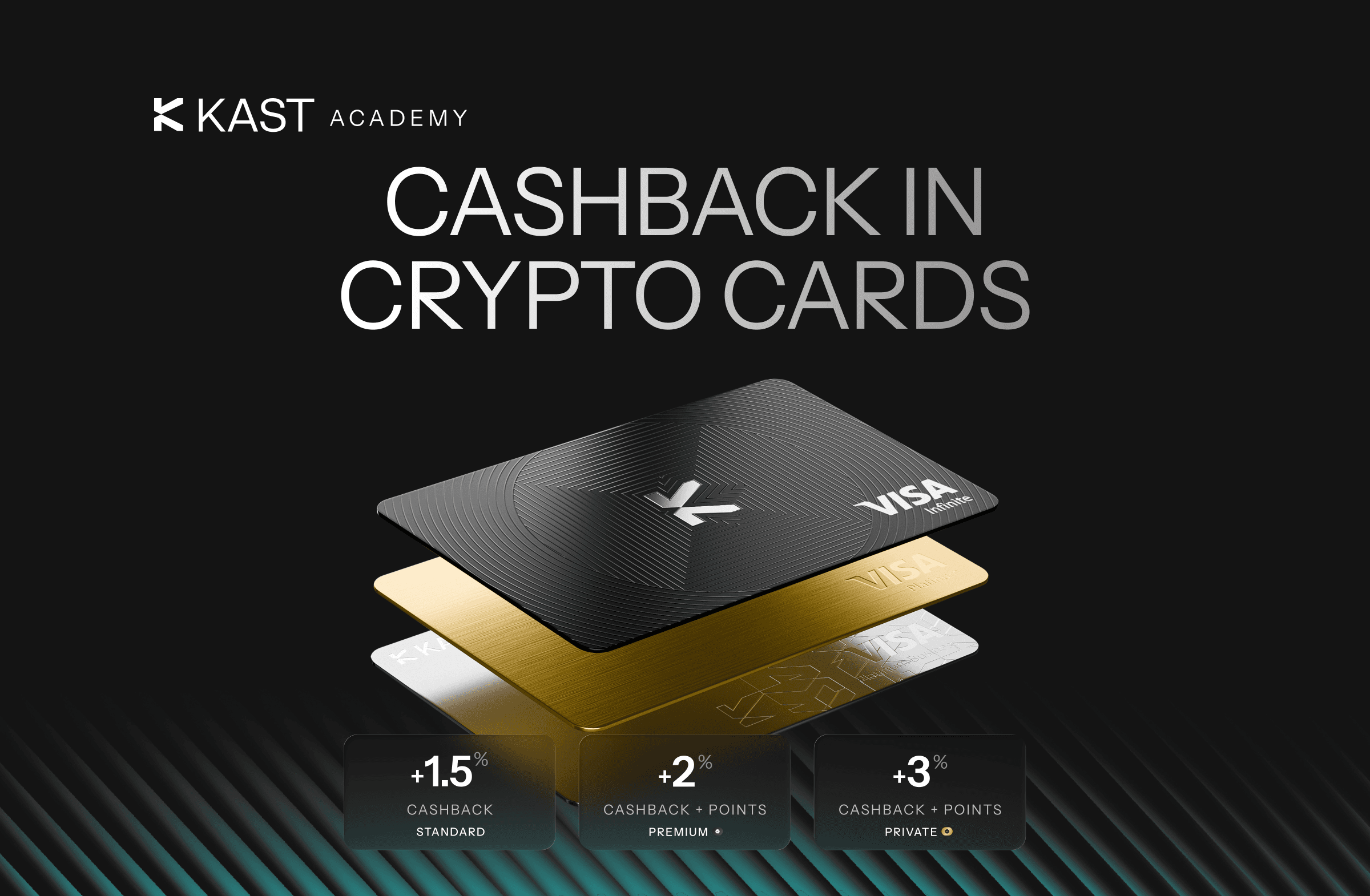

As you move up tiers, the rate improves and the earning range expands.

Private sits at the top, giving you 3% cashback. With Private, you also earn an extra 2% in KAST points across your spend, alongside your cashback.

You also get:

- 1 plated gold card included

- 2 additional free cards from any other tier

So when you evaluate Private, you’re comparing it to your current tier and asking:

On top of the perks, how much additional cashback does this upgrade generate compared to what it costs?

That’s the decision.

KAST Private Return on Investment (ROI) Examples

Let’s walk through a few realistic scenarios.

Not one ideal case. Not one cherry-picked number.

A few clear examples so you can map yourself into one of them.

Example: $20,000 Per Month

You’re spending $20,000 a month, which is $240,000 a year.

At 3%, that gives you $7,200 in cashback.

Now compare that to the fee. You pay $10,000 and get back $7,200, which leaves you at –$2,800.

On top of that, you’re also earning 2% in KAST points and getting free cards, which add additional value, but purely from a cashback perspective, you’re still below break-even.

So no, it doesn’t pay for itself at this level.

That doesn’t make it a bad tier. It just means cashback alone isn’t enough here.

Break-Even Point For KAST Private

Now find the point where cashback matches the $10,000 fee.

At a 3% rate, you need about $333,333 in annual spend.

That’s roughly $27,778 per month.

Here’s the math:

Around $27.8k per month, cashback alone offsets your costs.

Below that, you’re paying more than you get back. Above that, you’re ahead.

You still earn 2% in KAST points on top, plus the included cards, but this is the cashback baseline.

Example: $40,000 Per Month

At $40,000 per month, you’re spending $480,000 a year.

At 3%, that’s $14,400 in cashback.

After the $10,000 fee, you’re left with +$4,400.

You also earn 2% in KAST points on top, plus the included cards.

At this level, you’re clearly ahead.

Spend Levels Side By Side

The pattern is straightforward.

As your spend increases, the gap closes. Around $27.8k per month, it balances. Above that, it turns positive.

How To Decide

Keep this grounded in your actual behavior.

Start with your real monthly spend. Don’t use your best month. Take your last three months, average them, and adjust if something is changing.

From there:

- Multiply your monthly spend by 12

- Apply the 3% rate

- Subtract the $10,000 fee

That gives you your baseline result.

On top of that, you’re also earning 2% in KAST points, and you get the included cards, which add additional value. But the clean decision still starts with the cashback math.

One mistake to avoid is thinking in potential instead of reality.

If you normally spend $18k but assume you might spend more later, the numbers will look better than they actually are. The fee doesn’t adjust with your assumptions.

Consistency matters more than spikes.

Bottom Line

Is a $10,000 membership worth it?

It comes down to one thing:

Does your actual spending support the upgrade?

- Around $27.8k per month, you break even on cashback

- Above that, you’re ahead

- Below that, cashback alone doesn’t justify the fee

Everything else, including KAST points and included cards, sits on top of that baseline.

No complicated assumptions. Just your spend, your rewards, and whether the upgrade matches how you use the card.

Just your spend, your rewards, and whether the upgrade actually works for you.

Disclaimer: This content is provided by KAST Academy for educational purposes only and is not intended as financial advice or a recommendation to engage in any transaction. All information is provided "as-is" and does not account for your individual financial circumstances. Digital assets involve significant risk; the value of your investments may fluctuate, and you may lose your principal. Some products mentioned may be restricted in your jurisdiction. By continuing to read, you agree that KAST group, KAST Academy, its directors, officers and employees are not liable for any investment decisions or losses resulting from the use of this information.

Related articles

KAST Cards Explained: Tiers, Rewards, Fees, and How to Choose

KAST Cards have four tiers: Standard, Premium, Limited, and Luxe. Each changes KAST Points, SOL staking points speed, materials, and fees. Start with a virtual card in the app, then order a physical card with shipping where available.

How to Maximize Your KAST Membership: A Guide to the New Tier System

KAST Memberships v1.0 simplifies rewards by applying one tier across every card on your account. Instead of remembering which card does what, you choose a single annual tier that sets your cashback rate.

What is Cashback in Crypto Cards and How Does it Work

Crypto cashback looks simple until you realize “3% back” can mean three different things. This guide breaks down the common models and explains how KAST cashback works using a clear Locked → Redeemable → Redeemed lifecycle.