The Onchain Treasury Playbook: Balancing Yield and Liquidity

Moving money globally still runs on old constraints: cutoffs, intermediaries, and slow settlement. Onchain treasury changes that by using stablecoins to move dollar value 24/7 with clearer visibility into balances. This guide explains what changes and what the risks are.

Key Takeaways

- Onchain treasury is mainly about 24/7 settlement and real-time cash movement without banking cutoffs.

- Stablecoins can simplify global treasury workflows because they can move dollar-denominated value quickly, with timing that is often more transparent than traditional rails.

- KAST is one practical way to keep balances usable for payouts and spend, while also giving eligible idle USD a way to earn.

You’re not imagining it. Cross-border business payments still feel slower than the rest of your company.

You can ship code in minutes. You can hire someone in another time zone before lunch. But the moment you need to actually move money, everything slows down. Bank cutoffs. Delays with no clear explanation. Status updates that don’t really update anything.

That gap is the starting point for this guide.

Because the problem isn’t your process. It’s the infrastructure. Global money still runs on business hours, intermediaries, and systems that weren’t built for companies operating continuously across time zones.

So teams work around it. They pre-fund accounts. They hold buffers. They accept delays as normal.

Which leads to a quiet but expensive outcome: a lot of money sits idle just to keep operations running smoothly.

This guide breaks down how onchain treasury works, and how KAST lets you earn on balances without losing access to them.

Why Traditional Business Banking Breaks for Global Companies

Traditional business bank accounts weren’t designed for global operations.

They rely on intermediaries, regional infrastructure, and business-hour settlement, which creates friction for companies operating across time zones.

These constraints made sense at the time:

- settlement takes time

- banks need reconciliation windows

- intermediaries reduce risk

That structure worked when businesses were local or at least regionally focused.

It starts to break when your team, your customers, and your vendors are spread globally, and your operations don’t stop at 5pm in one timezone.

So treasury teams adapted. More accounts. More buffers. More coordination.

Not better. Not more efficient. Just more.

Why Stablecoins Improve Cross-Border Business Payments

Stablecoins didn’t show up as a “treasury product.” They showed up as a way to move money faster.

And once teams realized they could move dollar-denominated value in seconds, at any time, they started using them. Not because it’s new. Because it works.

Stablecoins are increasingly used as infrastructure for international business payments, because they allow companies to move dollar-denominated value globally without relying on traditional banking rails.

That alone is useful.

But the more interesting shift is what happens after the money arrives.

Because onchain, your “cash” doesn’t have to just sit there.

It can move instantly. It can be allocated programmatically. And in some setups, it can earn while it waits to be used.

That last part is the real difference.

In traditional systems, “liquid” and “productive” are often separate workflows. Moving between them usually creates delays, lockups, or operational overhead.

Onchain Treasury vs Traditional Business Accounts

At a practical level, the shift is simple:

Traditional treasury separates money movement and money productivity. Onchain treasury can keep both in the same system.

Instead of money sitting idle, then being moved, then maybe being invested somewhere else, you can keep balances closer to “ready state.”

You also get some operational upgrades:

- 24/7 settlement, not limited by banking windows

- real-time visibility into balances

- programmable workflows for approvals and transfers

Traditional vs Onchain Treasury Example

Let’s make this concrete.

Traditional setup:

You need to pay contractors in three countries on Friday.

So earlier in the week, you pre-fund multiple accounts. Some money sits idle waiting. Some gets stuck mid-transfer. One payment misses a cutoff and lands Monday. Finance spends time tracking where everything is.

Meanwhile, any surplus cash is sitting in separate accounts, not earning anything meaningful.

Onchain setup with stablecoins:

You hold funds in stablecoins.

Contractor payouts happen when you trigger them. You don’t have to plan around bank cutoffs in the same way, and settlement can be much faster depending on the route and network.

And the rest of the balance doesn’t have to sit idle by default. In some setups, it can be allocated into yield-generating strategies and pulled back when needed for payouts or spend.

Same money. Fewer steps. Less idle time.

This is where the difference becomes clear.

Traditional setups require multiple bank accounts, pre-funding, and coordination across regions.

Onchain treasury simplifies this into a single system where funds can move globally and remain usable at all times.

Stablecoin Yield: Where It Actually Comes From

Stablecoins are supposed to be boring.

But in modern treasury setups, they also introduce something traditional business accounts don’t offer: the ability to earn on idle balances without moving funds into separate systems.

So when you see “earn yield on USDC,” the obvious question is: where is that coming from?

Stablecoins themselves don’t generate anything. The yield only exists when they’re put to work.

In practice, that means your capital is being used. Borrowers pay to access stablecoins. Traders pay for liquidity so they can move between assets. Some strategies allocate into yield-bearing instruments like tokenized treasuries.

That’s the connection back to treasury.

Instead of cash sitting idle while it waits to be used, stablecoins can stay deployed in these markets and potentially earn until the moment you need to pull them back for payments or spend.

The important part is that this isn’t fixed or guaranteed. Yield moves with demand. When more people want access to stablecoins, rates go up. When capital is abundant, they go down.

Instead of asking "What's the yield rate", ask "what is my money doing right now", and can I get it back when I need it?

Two Core Types of Stablecoin Yield

To make this usable for treasury, it helps to separate two broad sources.

Reserve-Linked Yield (Indirect)

Stablecoin issuers often hold reserves in cash-like instruments, including short-term U.S. Treasuries. Those reserves can generate interest.

But as a default, that interest typically goes to the issuer, not the holder

In practice, companies may access reserve-linked economics through specific products, partnerships, or yield-bearing wrappers (depending on structure and jurisdiction).

Onchain Deployment Yield (Direct)

This is where most treasury-style yield strategies live.

Stablecoins get used in real markets:

- lending to borrowers who pay interest

- providing liquidity for trading

- allocating into tokenized real-world assets

Your capital is doing something. That’s why it earns.

Because it depends on usage, returns change over time.

What Good Stablecoin Yield Looks Like for Treasury

The question isn’t the highest rate.

It’s whether the setup works operationally.

A good yield setup means:

- you can trace the yield source

- you understand exit conditions

- you’re comfortable with risks

- you can monitor it without overcomplicating treasury

If you can’t explain it simply, it’s not ready for operating cash.

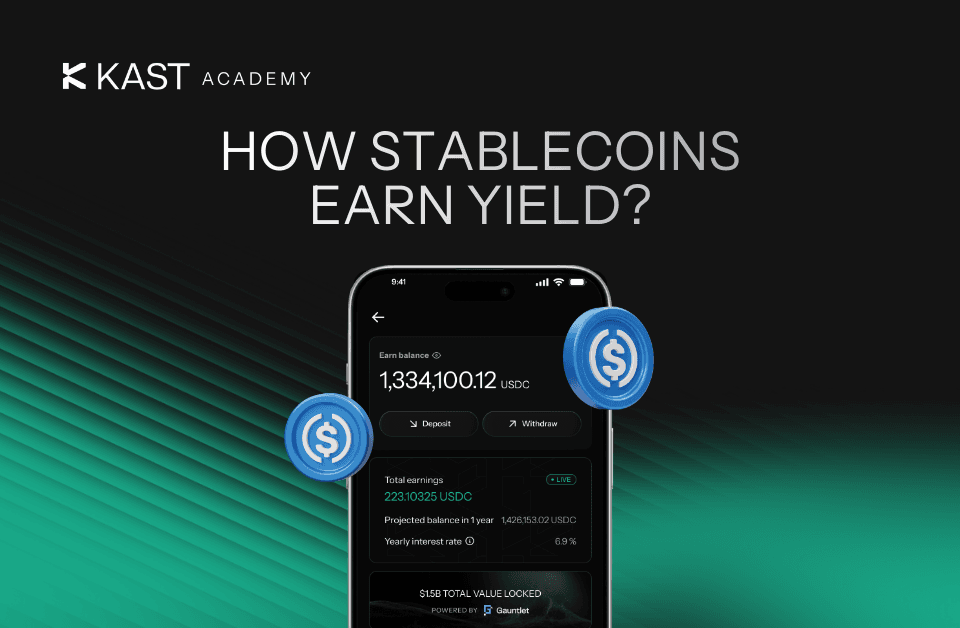

KAST Earn and Stablecoin Yield

Once you understand where stablecoin yield comes from, the next question is practical.

How do you access it without actively managing protocols every day?

In theory, you could do all of this yourself. Allocate across lending markets, monitor rates, manage rebalancing, track protocol risk.

In practice, that’s a lot of overhead.

That’s where something like KAST Earn fits in.

At a high level, it may route eligible USD balances into a managed onchain strategy so idle balances can potentially earn, subject to eligibility, jurisdiction, and risk.

A couple of expectations are worth being clear about:

- The APY is variable. It moves with supply and demand in the underlying markets.

- Earnings are auto-compounded. You won’t see daily payouts hitting your balance. Instead, your Earn balance grows over time, and you realize that yield when you withdraw.

The point is not “max yield.”

The point is: keep balances productive without adding operational overhead.

A Practical Onchain Treasury Model

Most teams end up with two layers:

- An always-liquid layer for operations: payroll, vendors, refunds. This needs to be predictable and accessible.

- A surplus layer where idle balances can be deployed into yield strategies until needed.

The key is not separating your world into a dozen disconnected systems.

It’s assigning roles to capital, and setting clear rules for how funds move between roles.

What Can Go Wrong With Onchain Treasury

Onchain treasury shifts risk. It doesn’t remove it.

Common categories include:

- Peg risk

- Liquidity and redemption risk

- Smart contract risk

- Counterparty risk

- Regulatory Risk

Then there’s infrastructure.

You’ll need to evaluate:

- cost

- speed

- reliability

- custody

- governance

That operational layer is what determines whether your setup actually works day to day.

Onchain Treasury Checklist

What This Looks Like in KAST Business

With KAST Business, the goal is simple: provide a global business account that supports real-time payments, while keeping balances usable and productive.

You keep funds usable for payouts and spend. And with KAST Earn, those same funds can generate yield until the moment you need to use them.

No separate systems. No extra steps.

Just a treasury setup where money stays liquid and productive at the same time.

What Onchain Treasury Actually Gives You

Traditional business banking hasn’t been broken. It’s been constrained by infrastructure that doesn’t match how global companies operate.

Onchain removes some of those constraints.

You still need discipline. You still need controls.

But you get something different in return:

- money that moves when needed

- money that stays visible

- money that doesn’t sit idle by default

Onchain treasury is emerging as a new model for global business accounts and cross-border payments, where money can move, stay visible, and remain productive at the same time.

Disclaimer: This content is provided by KAST Academy for educational purposes only and is not intended as financial advice or a recommendation to engage in any transaction. All information is provided "as-is" and does not account for your individual financial circumstances. Digital assets involve significant risk; the value of your investments may fluctuate, and you may lose your principal. Some products mentioned may be restricted in your jurisdiction. By continuing to read, you agree that KAST group, KAST Academy, its directors, officers and employees are not liable for any investment decisions or losses resulting from the use of this information.

Related articles

What Is RWA Backing? Tutorial on How Treasury Bills Secure Your Yield

Real-World Assets (RWAs) bring familiar assets like U.S. Treasury bills and bonds onchain. RWAs let you earn yield backed by traditional financial instruments. This guide explains how RWA backing works, why it exists in crypto, and how KAST Earn uses it to help you generate steady yield.

Where Does Stablecoin Yield Come From?

Stablecoin yield comes from real onchain demand, borrowing, trading, and capital deployment, not inflation or promos. When demand rises, yields rise. When it falls, so does yield.

APR vs APY: What’s the Difference and How to Compare Returns

APR and APY often look interchangeable, but they measure interest differently. APR is the annual rate before compounding, while APY is the annual return after compounding is included. This guide breaks down the definitions, gives an example, and explains how these mechanics show up in KAST Earn.